IRS Notice Help & Explanations

IRS Refund Offsets & Applied Credits Explained: CP 0049, CP 0080 & CP 0138

Few moments create more confusion than checking your tax refund status, expecting one number, and seeing another.

For many taxpayers, the first sign something changed is not a phone call or email. It is an IRS notice — CP 0049, CP 0080, or CP 0138 — explaining that part or all of your refund has been applied elsewhere.

Refund offsets and applied credits are not random decisions. They follow internal IRS procedures tied to outstanding balances, prior liabilities, or account adjustments. Understanding what happened is the difference between reacting emotionally and responding strategically.

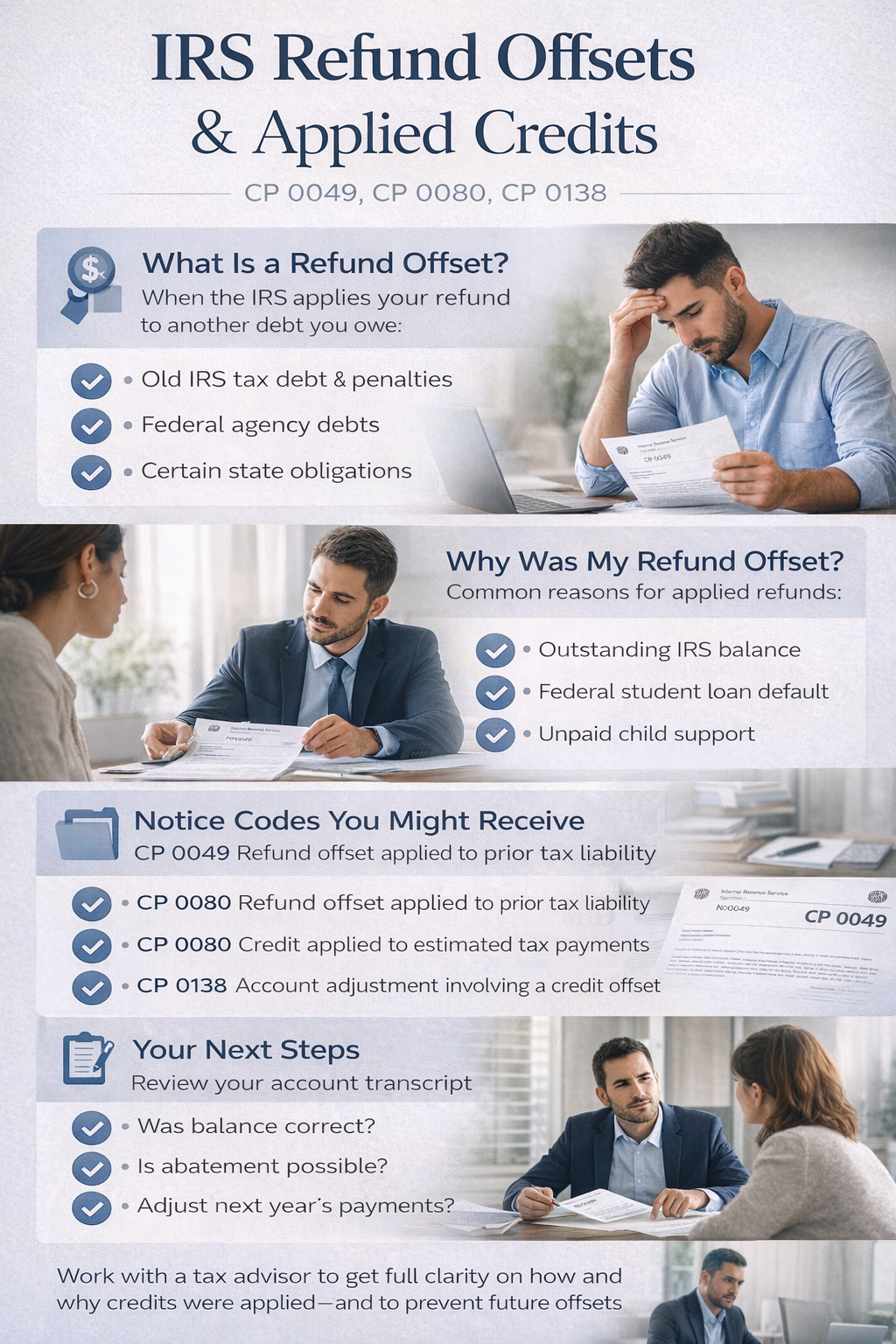

What Is a Refund Offset?

A refund offset occurs when the IRS takes an expected refund and applies it to another outstanding obligation.

That obligation may include:

- Prior year federal tax debt

- Penalties and interest

- Certain federal agency debts

- State tax obligations (in coordinated cases)

When this happens, the IRS sends a notice explaining how the refund was applied.

The refund is not “lost.” It is reallocated.

CP 0049 — Refund Applied to Prior Tax Liability

CP 0049 is one of the most common refund offset notices.

This notice informs you that your current-year refund was applied to a prior-year tax balance. Instead of issuing a payment to you, the IRS used the funds to reduce outstanding debt.

In many cases, taxpayers are unaware that an old balance still exists. Interest and penalties may have accumulated quietly over time.

CP 0049 is not an audit. It is an account adjustment reflecting debt satisfaction.

However, it raises an important question: Was the prior balance accurate?

Before accepting the offset as final, it is worth reviewing account transcripts to confirm that the prior-year assessment was correct and properly calculated.

CP 0080 — Credit Applied to Estimated Tax

CP 0080 typically indicates that the IRS applied an overpayment to estimated taxes rather than issuing a refund.

This often occurs when:

- You requested a credit forward

- The IRS processed a return showing a carryover

- Estimated payment allocations were adjusted

For business owners and self-employed individuals, CP 0080 may reflect quarterly planning decisions made at filing time.

The issue is not whether money moved. It is whether it moved intentionally.

If the credit was applied in error, correction requires timely communication.

CP 0138 — Account Adjustment Notice

CP 0138 is generally associated with account adjustments involving credits or offsets.

It may reflect recalculations, corrections, or application of funds to balances that were not previously resolved.

Unlike CP 0049, which clearly states that a refund was offset against prior debt, CP 0138 can feel less direct. It often requires careful review to determine exactly how funds were applied.

Again, this is not an audit. It is an administrative action.

But administrative actions can create long-term complications if left unexamined.

Why the IRS Offsets Refunds

The IRS is required by law to apply refunds toward certain outstanding federal debts before issuing payment.

This process is largely automated. Once a qualifying balance appears in the system, refund offsets are triggered automatically.

Taxpayers sometimes assume the IRS must notify them before offsetting. In reality, the notice typically arrives after the offset has occurred.

By the time CP 0049 or CP 0138 reaches you, the funds have already been applied.

The Risks of Ignoring These Notices

Refund offsets can mask larger account problems.

If a prior balance exists, questions arise:

- Why was it not resolved earlier?

- Has interest continued accruing?

- Are additional years affected?

- Could future refunds also be offset?

For small business owners, refund offsets can disrupt cash flow planning. A refund expected for reinvestment may suddenly disappear.

Ignoring the notice does not reverse the offset. It allows potential systemic issues to persist.

Is This an Audit?

No.

Refund offset notices are not audit triggers. They do not indicate an examination of your return.

They reflect account-level adjustments tied to existing balances or credit allocations.

However, unresolved balances can eventually lead to collection actions if not addressed. Offset notices are often an early stage in that progression.

Strategic Response Options

The appropriate response depends on whether the offset was correct.

If the prior balance was accurate, the offset may represent a positive step toward resolution.

If the balance was incorrect or miscalculated, action is required. That may involve:

- Transcript review

- Penalty abatement evaluation

- Account reconciliation

- Formal dispute procedures

For business owners, especially those managing multiple tax years, offsets can signal structural compliance issues rather than isolated mistakes.

This is where experienced analysis matters.

At Alpine Tax Resolution, cases involving refund offsets are approached methodically. Javier and the team begin with transcript analysis to confirm how and why funds were applied.

If the IRS action was appropriate, the focus shifts to stabilizing remaining liabilities.

If errors exist, corrective measures are initiated strategically, not reactively.

The Larger Financial Picture

Refund offsets are not punitive gestures. They are mechanical processes within a larger enforcement framework.

But mechanical processes can create cascading effects when underlying balances remain unresolved.

If a prior year tax liability exists, additional enforcement tools may follow:

- Balance due notices

- Installment agreement demands

- Collection letters

- Levy warnings in more serious cases

An offset is often the first visible sign of an unresolved issue.

Handled properly, it can be the beginning of a comprehensive resolution strategy rather than a financial setback.

Final Perspective

CP 0049, CP 0080, and CP 0138 are signals.

They indicate that your IRS account is active and that funds have moved in response to existing balances or credit allocations.

Understanding what happened — and verifying that it happened correctly — restores control.

Refund offsets can be routine. They can also reveal deeper account problems.

The difference lies in analysis.

Alpine Tax Resolution handles these matters with discretion and precision. Every case begins with review, confirmation, and strategic planning before any action is taken.

Refunds should never feel mysterious.

Clarity is the first step toward resolution.

Have questions or need guidance? Send us a message and our team will reach out with next steps...

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.